The numbers don’t lie, and they’re talking trends.

If ever there was a sign that the fashion industry as a collective is putting the focus on looking and moving forward it was the Haute Couture collections held in Paris this month. In real life presentations showcasing creativity at its best to in real life Couture goers and front rowers. Whilst we won’t all be wearing the luxury of couture, our wardrobes have thankfully not been relegated to a stay-at-home groundhog day of not-so-elevated well-worn tees and comfy tracksuit pants. Fashion has held up a mirror to every socio-political-economic crisis throughout history, both during and after. 2020-2021 has been no different. So where have our post-pandemic hemlines and relegated-to-the-fashion-sidelines been heading post lockdown?

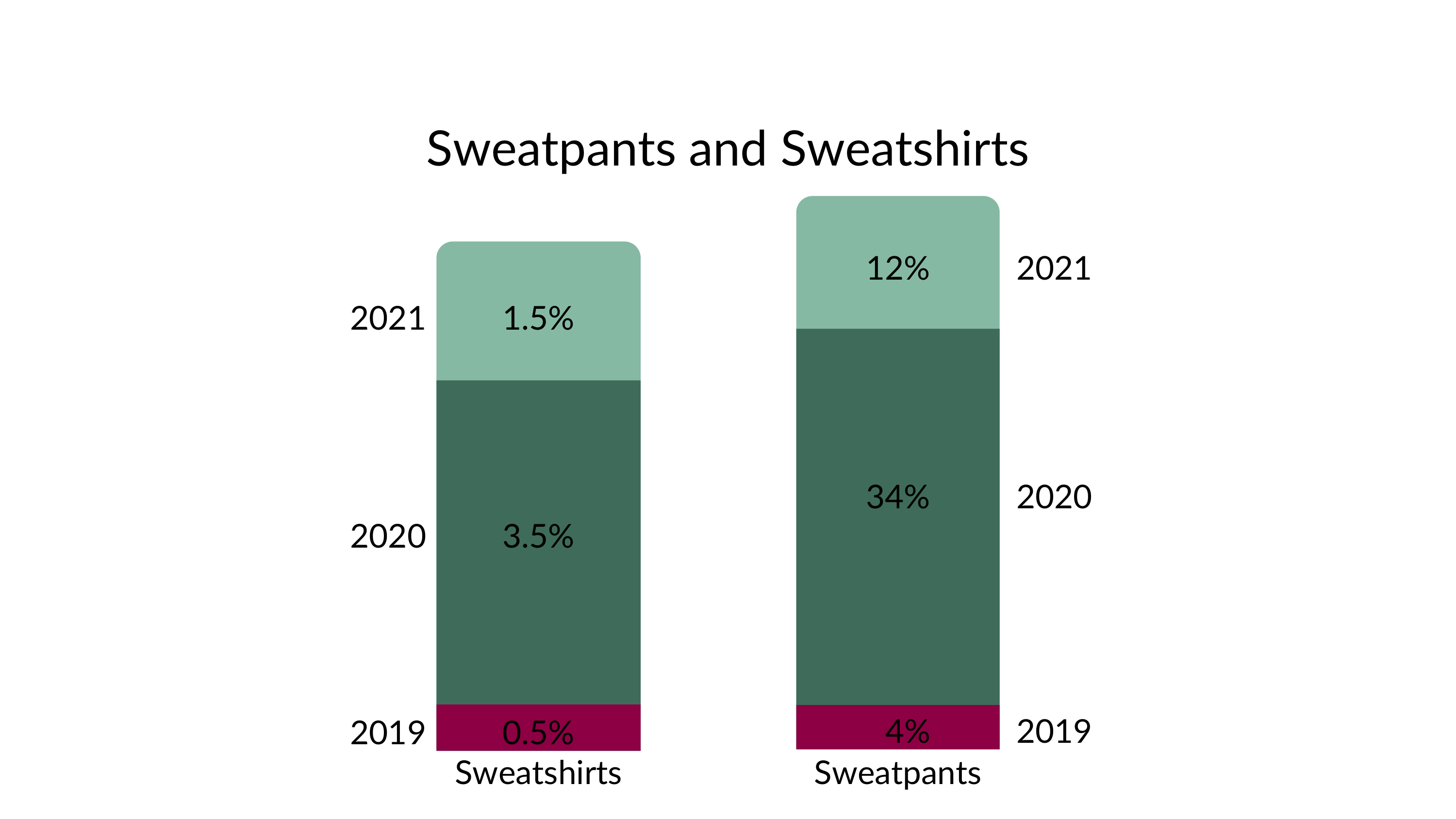

Thanks to the Diana effect (remember her Harvard sweatshirt and cycling shorts gym combo) discovered by a new generation of Tik-Tokers, and the dress-down glamour trend seen everywhere on the spring/summer catwalks from Celine to Prada and Gucci, you can hold onto and breathe new life into those beloved sweatshirts and tracksuit pants. Sales of sweatshirts tripled in volume compared to the same period in 2019 with a peak of 3.6% of total women’s spend mid lockdown. With a similar story for sweatpants. Coming out of lockdown this has been less about lounging about at home and more about the fact that spring/summer trends saw athleisure reworked into new ‘ways to wear’, from day to hybrid office/home working looks, to dressed-up for night. Sweatshirts have been cropped, mixed and matched, tie-dyed, embellished every which way; the opportunities are endless. Even pre-2020 the move towards athleisure by night - just add a disco diva heel and a sequin or two - was already taking shape over at the likes of Tom Ford.

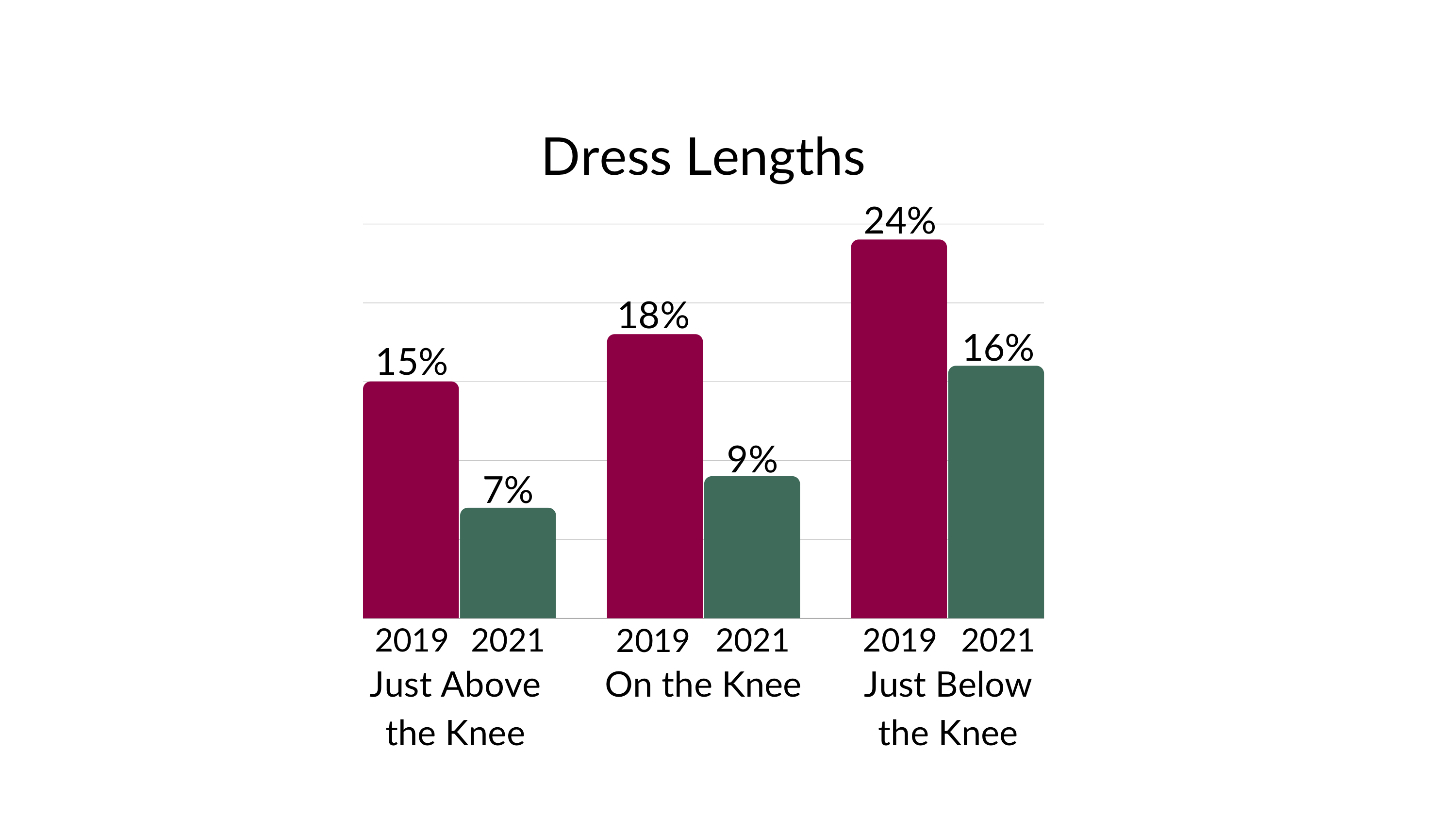

Whilst Mary Quant gave us rebellious miniskirts in the 60s, hemlines haven’t necessarily been rebelling over the last year when it’s come to a shift in what we’re buying. Circumstances have dictated that there’s been not much need for knee-length dresses or skirts (especially pencil skirts). These lengths are usually associated with workwear and occasion wear (occasionwear has seen a hit from 24% to 10.28%).

On the knee dresses have dropped from 18% to 9% and just above the knee dresses saw a decline in sales from 15% to 7%. This ‘no need for workwear’ has also been reflected in trouser styles: tailored trousers have dropped from 24% to 13%. It’s not surprising that wide leg, more relaxed fit trousers were one of the key catwalk trends this season.

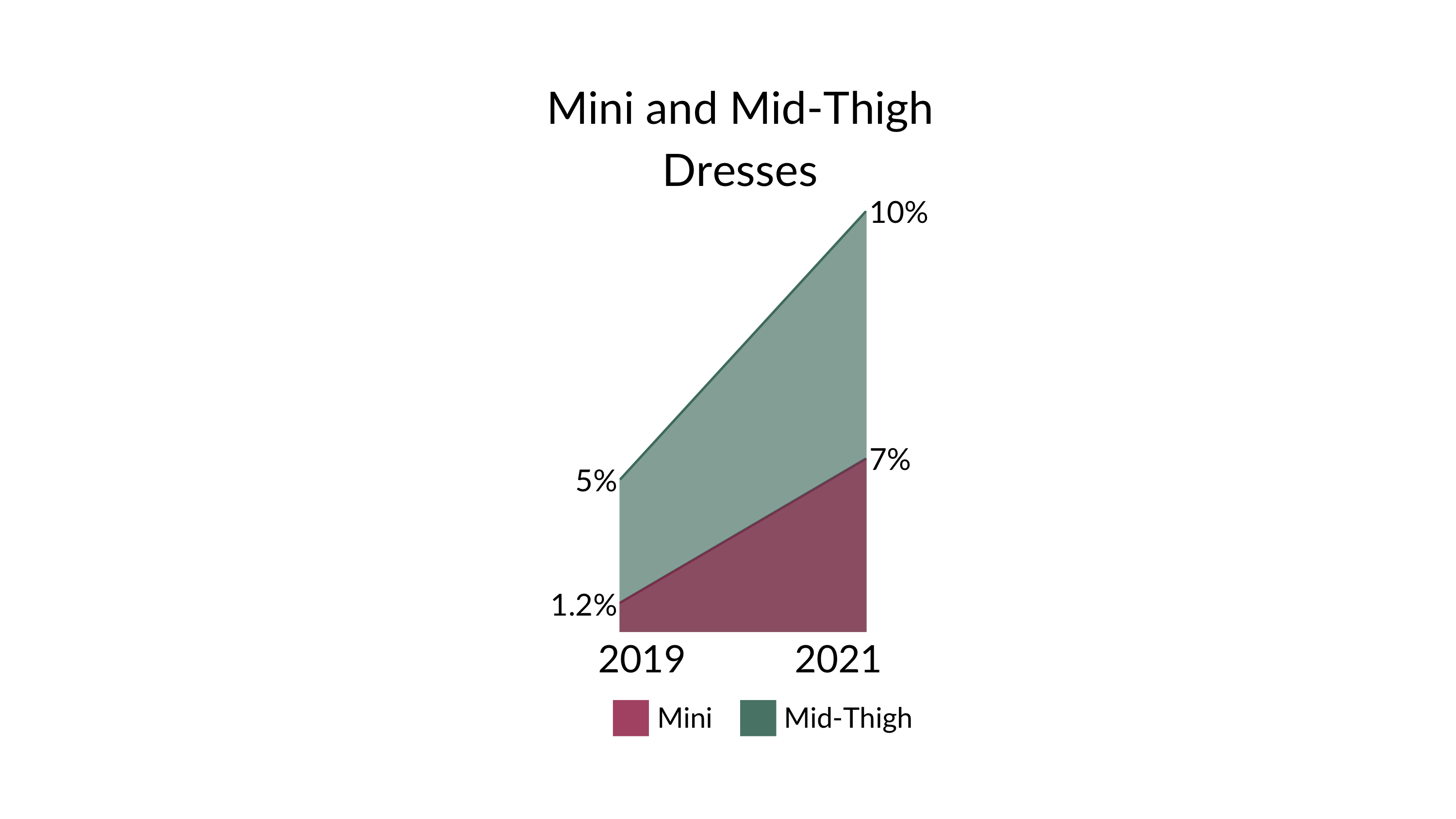

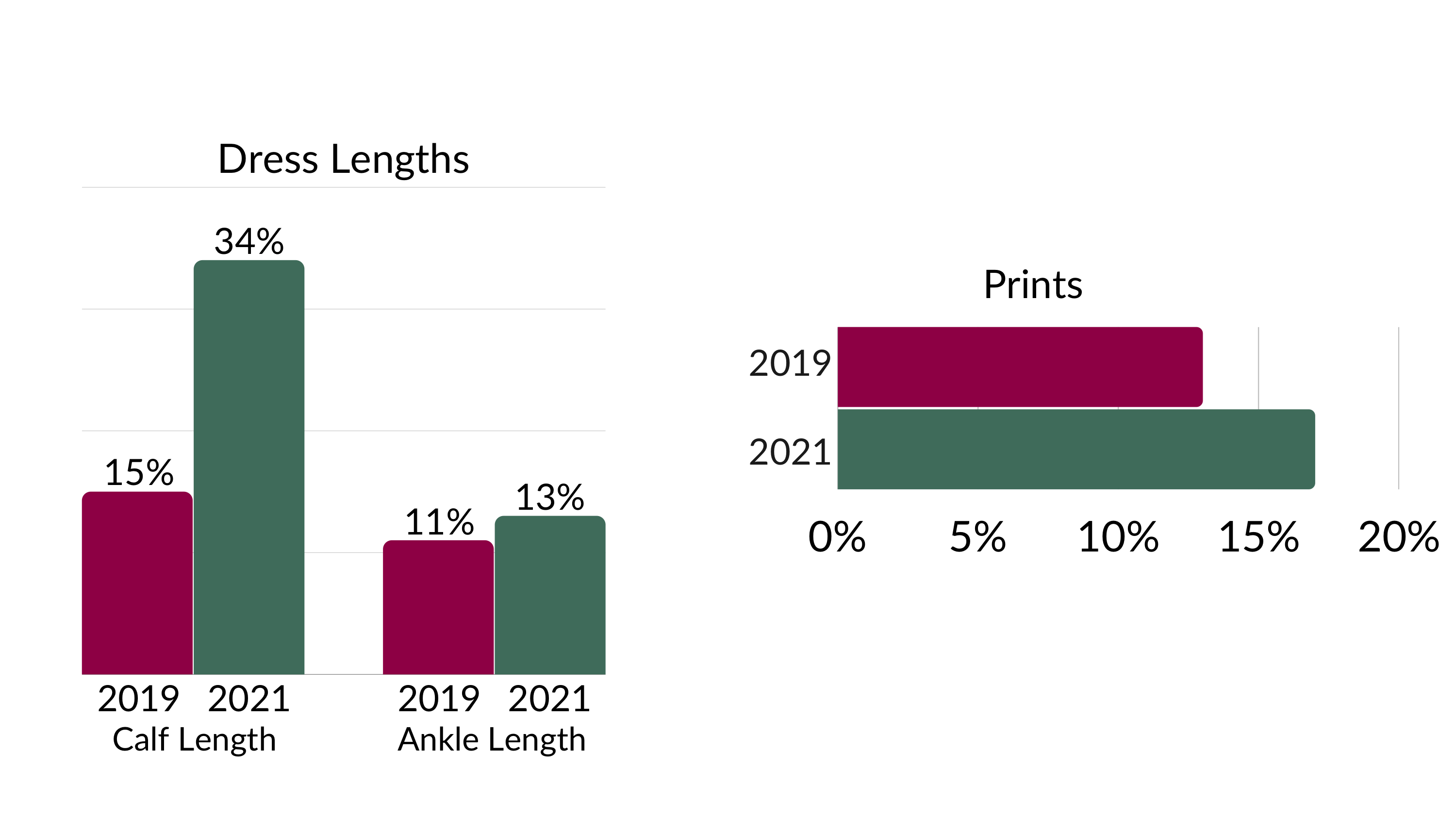

What has been happening with the length of dresses is that the middle-man so to speak has been knocked out. Hemlines have gone up and down but nowhere in-between. This has a lot to do with the rise and rise and rise of the floaty, puff sleeve midi-dress styles that we’ve seen in summer fashion for some time now, ditto cute little smock dresses, the much loved tea dress and the popularity of the house dress. Our data shows a big swing to calf length dresses from 15% of all dress purchases to a staggering 34%. The mini length has jumped from 1.2% to 5%. And whilst florals are not necessarily ground breaking for spring or summer, they’re up on 2019 (13% to 17%)

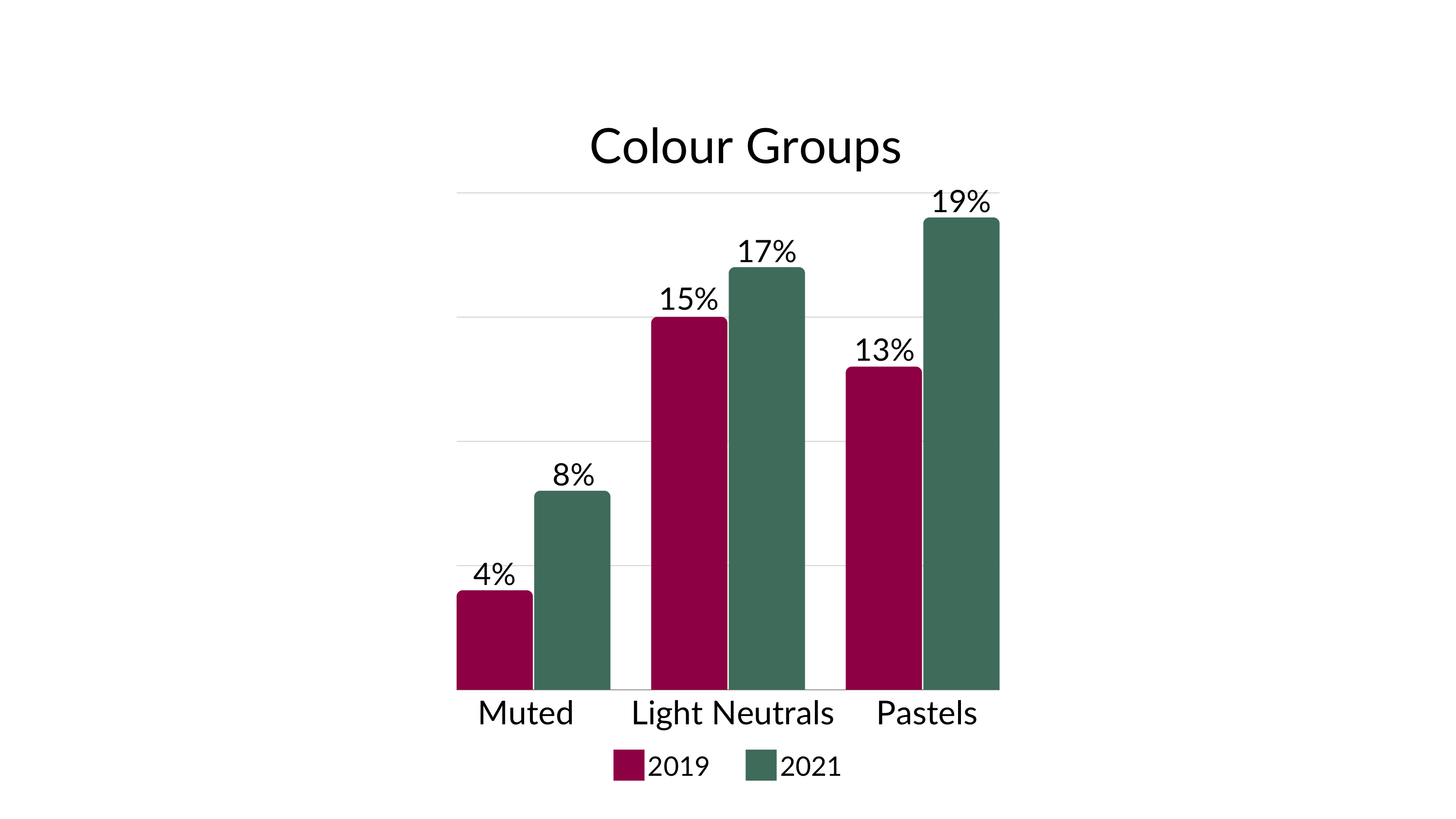

Spare a thought for dresses in those hot summer brights, it’s time for the quieter shades with pastels rising from 13% to 19% and a rise for muted shades from 4% to 8%. Although if you’re after a must-have summer suit then a bold red or happy green are your go to colors. Or you can always wait until next season, because obviously like all good things in fashion it changes. It wouldn’t be fashion otherwise.